When I started in insurance, in 1988, one of the first things I learned about was “risk” and how it is dealt with.

Risk is the probability that something bad will happen. People deal with risk in one of two ways. Either they “retain” the risk and pay the bills out of their own pocket or “transfer” the risk to someone else.

Health insurance is a “risk-transfer” strategy. The insured pays the insurance company a “premium”. In return, the insurance company promises to pay medical bills in the future.

The problem is that while the Basic plan allows an individual to transfer the bulk of large medical bills to an insurance company, deductibles, co-insurance, penalties and co-pays require the insured to retain the financial risk for smaller medical bills. It is this set of medical bills that often cause a problem after an illness.

In this book I will share various strategies that can be used to deal with the “risk” of medical bills in the future.

Sadly, there is so strategy that will cover all of the financial risks, and troubles, that can be caused by a serious illness. However, in these pages you will find several strategies that you can use to transfer much of the financial risk.

The basic strategy is the one that is most popular. Politicians and media have tried, for years, to convince Americans that it is all that is needed. Sadly, the statistics do not support their conclusions. In 2022, I read where more Americans had health insurance than at any time in history. Two days later I read where 60% of adult Americans either cancelled or post-poned getting medical treatment because of the cost.

If both statements are accurate, the only conclusion possible is that the Basic approach still falls short.

One of the issues that I find appalling is that even in an America where more people than ever have “health insurance” we still have a society where people cannot afford to pay medical bills. That problem is a result of not fully understanding how much a deductible and co-insurance can hurt your wallet.

Sadly, many people elect to use plans with a high deductible because they are the least expensive. That strategy is just fine until somebody gets sick or injured and the deductible is so high that they have to pay 100% of the health-care bills out of their pocket, even though they have “health insurance”.

Yes, basic plans will pay many medical bills but not all of them. Because of the limitations that are in Basic plans, it is still important to add specific benefits to a Basic plan if you want insurance to pay for all your medical bills.

Traditionally an entire family was on the same health insurance policy because employers would often pay for coverage for the entire family. This is a hold-over from World War 2 when employers were not allowed to give raises to keep and motivate employees so the practice of paying for “health insurance” for the family was begun.

Sadly, even before Health Care became a political tool, many employers had stopped paying for dependent health insurance. That trend just increased after the ACA became law.

As health insurance premiums increased, and more federal regulation were placed on group health insurance fewer employers paid for dependents. Today it is the exception and not the rule for companies to pay for health insurance for dependents.

Employers still pay a portion of the premium for employees since they can “write off” that cost from their taxes as a business expense, but they often do not pay any of the premium for the employee’s family.

Here is the irony. The law requires groups to offer coverage for dependents. However, the same set of regulations forbid IRS help with premiums for those who are eligible for group health insurance, whether they participate in the group or not.

In other words, under current rules, if a dependent is even eligible to be covered on a group plan, that individual is ineligible for any help with their health insurance premium from the government. They either have no choice but to pay the full premium for the group plan or the full premium for the ACA plan.

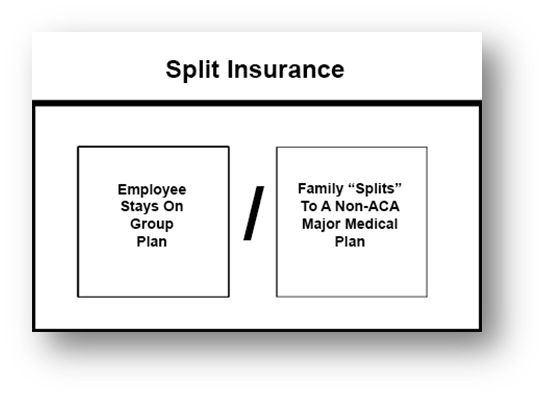

Considering recent changes to health insurance, the Split-Insurance strategy can be used by families where one parent/spouse works for a company that sponsors a group health insurance plan.

The ACA requires employers who offer group health insurance to pay, at least, 50% of the premium for employees but there is no mandate for the employer to pay anything for the family.

When the Split-Insurance strategy is used, the employee is “split” away from the rest of the family. The employee stays on the group plan and his/her premium is subsidized by the employer.

The dependent family members enroll in a less expensive, non-ACA plan.

This strategy will still not allow people to participate in IRS tax credits to help with health insurance premiums.

However, unsubsidized dependent coverage, on a group health plan, is often quite expensive. When that is the case, the Split Insurance strategy can help a family save several hundreds of dollars in premium each month.

When the politicians formed what was to become the ACA they promised to make the cost of health insurance more in line with what younger folk paid. They thought they had done this by lowering the ratio that insurance companies could charge to older, sicker folk as compared with younger, healthier people.

Before the Affordable Care Act insurance companies were free to charge older people 5 times what they charged younger folk. Under the ACA insurance companies can charge older people no more than 3 times what they charge younger people.

Early in my career I was taught, “No politician is able to make a law that insurance companies cannot adjust to.” Sadly, that prophecy came true regarding older Americans.

People thought that what would happen is that insurance companies would lower the premiums for older people. What really happened was that insurance companies raised premiums for younger folk so that they could continue to charge older people more money.

The result is that older people are still paying high premiums for health insurance. The only effect the ACA had was to drastically increase how much younger people have to pay for “health insurance”.

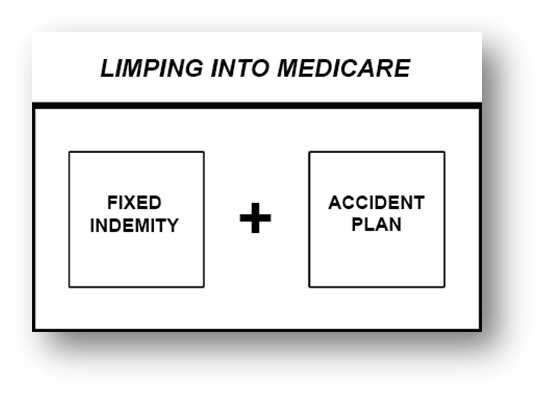

The “Limping Into Medicare” strategy is not right for everyone. I only use it with people over the age of 60 but not quite eligible for Medicare.

This strategy, while normally less expensive than a non-subsidized ACA plan, requires the insured to retain a little more risk. It is not a strategy for anyone who is risk adverse.

“Limping Into Medicare” requires an individual to use a Fixed Indemnity plan along with an Accident plan. The key is to use a fixed indemnity plan that has a benefit hat is high enough to pay hospital, testing and doctor bills. That way they have coverage for expensive stays in a hospital or when using an ER because of an accident. It is closer to what was originally intended for health insurance before all the “Bells & Whistles” were added over the years.

As mentioned before, these plans have no, or a nominal deductible, depending on which plan is used.

I call this strategy, “Limping Into Medicare” because it does not provide the same benefits as ACA plans provide. Some benefits are actually more generous, and some ACA mandated benefits are missing. However, the “Limping Into Medicare” strategy is generally much easier on the wallet than an ACA plan for someone who only gets a token amount of “help”, to pay the premium, from the government.

In my opinion, it provides better benefits than ACA plans for accidents or hospitalization, but it is not as generous for out-patient surgery, cancer or chronic disease that requires frequent monitoring visits to a doctor.

There is a potential safety-net for those who elect to use the “Limping Into Medicare strategy. The strategy is acceptable for healthy older Americans, but if they are diagnosed with a problem, later in the year, they can still enroll in an ACA plan during the next enrollment period.

Since an Open Enrollment Period, for ACA plans, is required each year, the worst someone who uses the “Limping Into Medicare” strategy risks is a delay of one year until they can get an ACA plan.

However, in years when they enjoy average health, they can save money if they are not eligible for tax credits to help pay for health insurance premiums.

Everyone alive risks cancer, heart attack or stroke. Unfortunately, it is one of the hazards of life.

However, as I understand genetics, those who have had a parent or sibling experience one of these diseases is at an even higher risk.

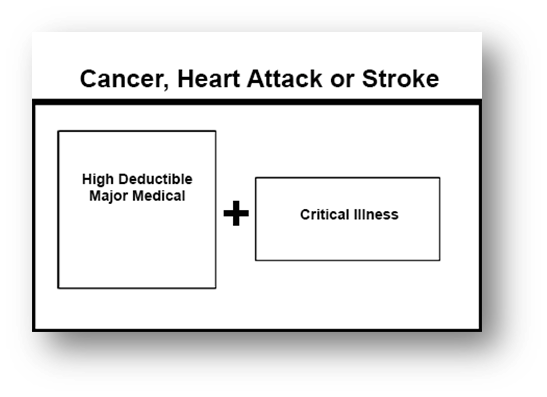

I do not routinely mention this option to my clients when I first speak with them. Perhaps I should, but in my opinion, Major Medical insurance is already too expensive. Typically, I only suggest this strategy to people who volunteer that they have a higher than normal concern about cancer, heart attack or stroke, or that they have family members who have been treated for one of these serious medical problems.

This strategy is not right for everyone, but for those who are concerned, it can eliminate most, if not all of the costs associated with cancer, heart attack or stroke.

The stratgey can be used with either an ACA or Non-ACA medical plan. Typically, I add an Accident Supplement to the Major Medical plan so that in the event of an accidental injury, the client does not have to deal with a deductible. However, the Accident Supplement is not required for this strategy to work.

Whether an ACA or Non-ACA Major Medical plan is used makes no difference. Just be certain that whatever Major Medical plan is used will cover treatment for cancer, heart attack or stroke after a deductible.

Whatever Major Medical plan is used, elect the highest deductible available. You will then obtain a Critical Illness plan with a benefit that is at least equal to the maximum out-of-pocket expenses that your plan requires.

Also, it is important to remember that cancer, heart attack and stroke often have lenghthy recovery times. Although it is not required, if your personal saving are not sufficient to allow you to remain in your current standard of living, it is wise to increase the benefit for 3-6 months worth of living expenses.

Often, but not always, the total amount of benefit needed from the Critical Illness plan is $20,000 – $30,000.

In the event of a diagnosis of cancer, heart attack or stroke, 100% of the medical bills will be paid plus there will be money available to hel pay other bills while you recover from treatment.

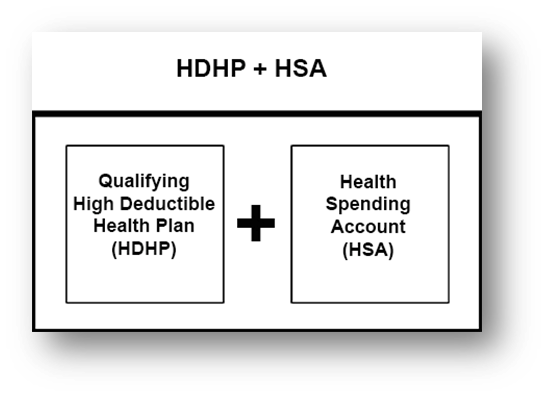

Perhaps the most well-known health insurance strategy is the High Deductible Health Plan with a Health Saving Account. It is a plan that has been made popular in America by wealthy politicians. At first glance it is very attractive, but this strategy does have some draw-backs.

The IRS has determined what benefits a health insurance plan may have to be qualified for the HDHP + HAS strategy. Not all high deductible health insurance plans qualify. In fact the only plans that qualify are only ACA compliant plans, and even then, just because a plan has a high deductible does not mean that it will qualify.

When you review your options, within the ACA, you will notice that plans that are qualified for use with this strategy are clearly indicated.

Once one is enrolled in a qualifying High Deductible Health Plan, that person is allowed to contribute a limited amount of money, on a tax-favored basis, to a Health Savings Account (HSA).

The idea is that when a person has a medical claim, they will use the money in the HSA to pay their bills with tax-favored money. Any money that is left in the HSA continues to grow on a tax favored basis.

WARNING I: In spite of what wealthy politicians say, this strategy has limited application. In my opinion, it is only good for people who are looking for additional tax deductions.

I am an insurance professional and not a tax advisor. All I can do is give my opinion. In my opinion, there are better strategies that one can use if they claim just the Standard Deduction on their tax return. This strategy is best for people who have enough deductions to file an itemized tax return.

Before using this strategy, make certain to discuss it not only with an insurance professional but your trusted tax adviser.

WARNING II: My experience is that many people who use this strategy do so because of the lower cost of the High Deductible Health Plan and forget to open up and fund a Health Savings Account.

When that happens, not only are there no tax benefits, but there is no money to pay for medical bills before the high deductible has been met. People who fail to fund a HSA must use money from their discretionary funds to pay for unexpected medical bills.

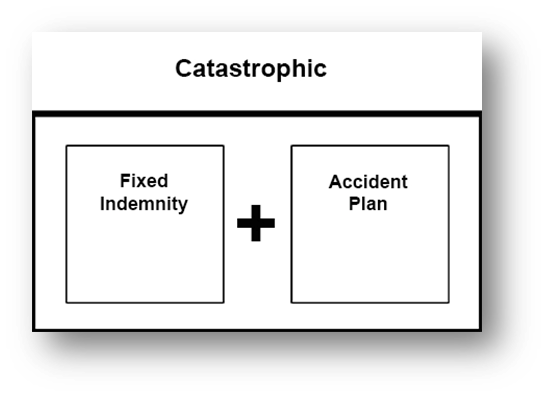

Some people do not want to pay for a comprehensive health insurance policy. They prefer to self-insure/pay for routine medical bills out of their pocket and only pay for health insurance that is used for very expensive medical bills.

Technically, there is no definition of what is included in a catastrophic type of plan. Therefore, the principle of “caveat emptor” (let the buyer beware) comes into play when this strategy is used.

If you elect to use this strategy, make certain that you understand exactly what your plan will, and will not, cover and what is required on your part.

Sadly, I am often told that people want a “Catastrophic” type of plan and only when a claim is denied will that person understand how important it is to review the benefits and exclusions for their plan before they commit to a “Catastrophic” type of plan.

When I am asked for a “Catastrophic” type of plan, I prefer a portfolio as illusrated above. The Fixed Indemnity plan, that I deal with, includes benefits for both expensive overnight stays in the hospital, with no deducible and partial coverage for a limited number of routine visits to a doctor’s office or Urgent Care clinic.

The plan that I use has some coverage for accidents but, in my opinion, not enough. In addition to the Fixed Indemnity portion of the plan I recommend an inexpensive Accident plan, that is available on a stand-alone basis.

That way, if the client suffers an accidental injury they can go straight to the ER, to get help, without having to worry about money.

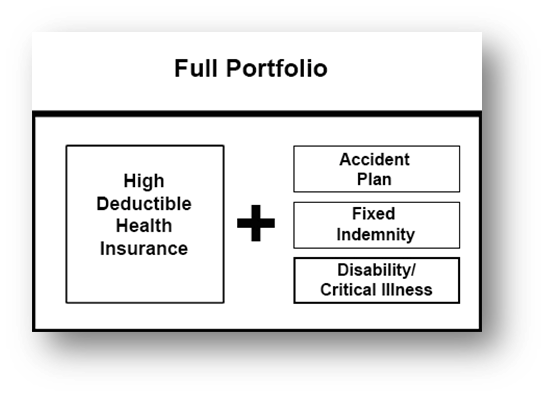

The Full Portfolio strategy can be used by people who want as little risk as possible if they get sick or injured. Some of the plans are available as guaranteed issue policies while some of them are subject to medical underwriting.

A ”portfolio” is a group of related documents. That relationship is what gives this strategy its name.

The portfolio is built on the foundation of a solid Major Medical plan with a high deductible. If you can qualify for Tax Credits to help with the cost of health insurance, you can use an ACA compatible plan. However, if you do not qualify for Tax Credits, you can still form a portfolio with a Non-ACA plan. Just keep in mind that in that case there is no coverage for routine maternity costs or substance abuse.

Once the base Major Medical plan has been established, the client will add an Accident plan and a Fixed Indemnity plan to pay for overnight stays in a hospital and ER treatment for accidents that are subject to the Major Medical deductible.

Depending on which Fixed Indemnity policy is used, there may also be help with the bills for routine visits to a doctor’s office.

Some, but not all, Fixed Indemnity policies also have benefits for out-patient surgeries that would be subject to the Major Medical deductible.

When using this strategy, if the goal is to get as comprehensive insurance as possible, research how much your hospital charges per night. If possible, get a Fixed Indemnity plan that will pay you enough to pay the potential hospital bill plus enough to pay for other charges you may get from your doctor.

The Disability or Critical Illness policy will give you some money that is paid directly to you, while you are at home recovering from medical treatment.

Medicare Disclaimer

“We do not offer every plan available in your area. Any information we provide is limited to those plans we do offer in your area. Please contact Medicare.gov or 1-800-MEDICARE to get all of your options.”

Want more information? Text 903-335-1969 or use the contact form below.